Global equity markets rallied strongly last week as a proposed two-week ceasefire framework in the Middle East improved investor sentiment and pushed oil prices sharply lower.

Japanese equities led the gains, while UK equities also rose but underperformed global peers.

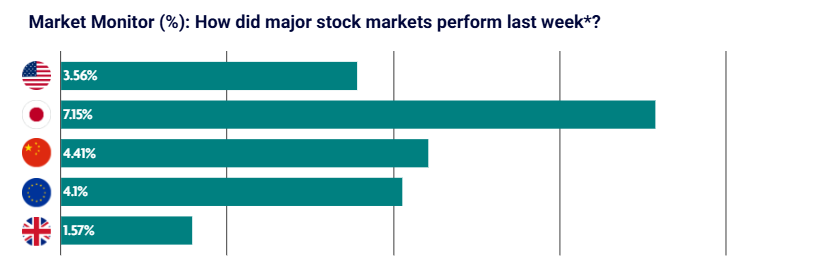

US: Equities jump on two-week ceasefire framework

U.S. equities recorded a second consecutive week of strong gains as signs of de-escalation in the Middle East supported risk appetite.

Markets began the week cautiously, but sentiment improved sharply following reports of a proposed two-week ceasefire framework. Oil prices, which had surged in recent weeks, fell heavily on Wednesday, marking their largest daily decline since 2020.

The Nasdaq led gains, supported by continued enthusiasm for artificial intelligence and semiconductor stocks. Energy was the only sector in the S&P 500 to fall. All major U.S. indices rose by more than 3% over the week.

Economic data was less supportive. Inflation rose sharply, driven mainly by higher fuel prices, while core inflation increased more modestly. Growth data was revised lower, services activity slowed, and consumer sentiment weakened significantly as households became more concerned about price pressures.

Japan: Equities stage relief rally

Japanese equities rebounded sharply, with the Nikkei rising by more than 7% as exporters and technology stocks rallied following reduced fears of a worst-case geopolitical outcome.

The Japanese government announced a further release from strategic oil reserves to support domestic energy supply, building on earlier stockpile measures.

Higher energy prices fed through into producer prices, which surprised to the upside. At the same time, real wage growth improved, although consumer confidence deteriorated sharply as fuel costs remained elevated.

China: Producer prices rise for the first time in over three years

Chinese equities ended the holiday-shortened week higher, supported by easing geopolitical tensions and a notable improvement in producer prices.

Producer price inflation turned positive for the first time in more than three years, driven primarily by higher energy and commodity costs rather than stronger domestic demand. Consumer inflation, however, eased.

Regulators introduced tighter short-term trading rules for major shareholders and executives in an effort to reduce speculative behaviour and improve market discipline.

Separately, President Xi hosted Taiwan’s main opposition leader in Beijing in a rare diplomatic meeting, highlighting increased cross-strait tensions ahead of further high-level engagements.

Europe: Markets rise despite weaker growth outlook

European equities advanced strongly as markets responded positively to confirmation of a two-week ceasefire agreement between the U.S. and Iran.

Germany’s DAX rose 2.74%, Italy’s FTSE MIB gained 4.35%, and France’s CAC 40 increased 3.73%.

Despite the improved market tone, the European Union warned that it is preparing to cut its 2026 growth forecasts, citing stagflation risks created by weaker growth and rising inflation linked to geopolitical instability.

Economic data remained mixed. German factory orders rose modestly but missed expectations, while services activity contracted again in France and Italy.

UK: Equities rise but lag global peers

UK equities also moved higher over the week, though they lagged behind other major markets.

Prime Minister Keir Starmer pledged to strengthen Britain’s economic resilience, but investors appeared unconvinced, with the rally in gilts proving short-lived. This suggests markets still see the UK economy as particularly vulnerable to higher energy prices.

UK house prices rose 0.8% year on year in March, according to the Halifax House Price Index. This marked a slowdown from February’s 1.2% increase and came in below expectations for 1.5% growth.

In separate news, UK financial regulators are in discussions with the government’s main cyber security body and major banks to assess the risks posed by Anthropic’s latest AI model, which has demonstrated advanced capabilities in identifying cyber vulnerabilities.