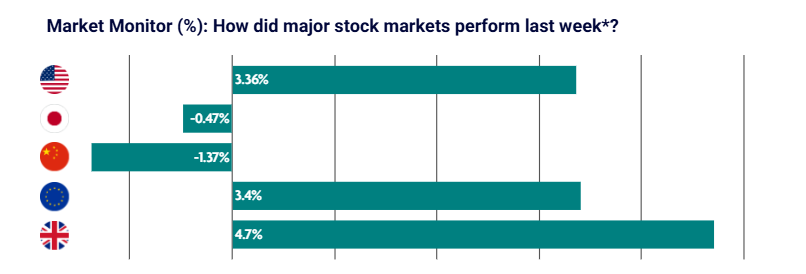

Global equity markets were mixed last week, with sentiment shifting as comments from U.S. President Donald Trump raised hopes of a near-term resolution in the Middle East.

U.S. and European equities rebounded strongly, while Japanese and Chinese markets lagged as energy and geopolitical concerns continued to weigh.

US: Equities rally on hopes of de-escalation

U.S. equities finished the shortened week higher despite ongoing geopolitical uncertainty.

The Nasdaq recorded its strongest weekly performance since November, while the S&P 500 also rose sharply. Smaller companies advanced as broader market participation improved.

Markets rallied midweek after comments from President Trump raised hopes that tensions in the Middle East could ease. However, gains were briefly tested after a later speech failed to provide a clear timeline for de-escalation, pushing oil prices higher and weighing on equities before markets recovered into the close.

Economic data was mixed. Private payroll growth exceeded expectations and jobless claims declined. However, job openings and hiring slowed. Consumer confidence rose modestly, and manufacturing activity expanded for a third consecutive month, although employment continued to contract and price pressures increased.

Japan: Energy concerns weigh on equities

Japanese equities declined, reflecting sensitivity to rising oil prices and geopolitical uncertainty.

The Nikkei fell 1.7% as concerns grew around energy security and the potential disruption to shipping through the Strait of Hormuz.

Markets increasingly priced in a potential Bank of Japan rate rise in April, with bond yields moving higher. The yen strengthened slightly amid speculation of possible currency intervention.

Inflation data in Tokyo came in marginally below expectations. Industrial production met forecasts, while retail sales disappointed.

China: Mixed performance as domestic data improves

Chinese equities delivered mixed performance as stronger domestic data helped offset broader geopolitical risks.

Purchasing Managers’ Index readings improved across both official and private surveys, suggesting stabilising economic activity. However, rising input costs pointed to increasing margin pressures for businesses.

China, alongside Pakistan, called for a ceasefire in the Middle East, highlighting concerns around energy infrastructure and global shipping routes.

Separately, China removed export tax rebates on several clean energy products from April, a move expected to increase cost pressures and accelerate consolidation within the sector.

Europe: Equities rise despite inflation pressures

European equities rallied strongly as optimism grew that tensions in the Middle East may ease.

Germany’s DAX rose 3.89%, Italy’s FTSE MIB gained 5.18%, and France’s CAC 40 climbed 3.48%.

Inflation in the eurozone increased to 2.5%, the highest level since early 2025, driven largely by a sharp rise in energy prices of 4.9%.

Economic growth expectations weakened in Germany, with leading institutes cutting their 2026 GDP forecast to 0.6%. Manufacturing trends varied across the region, with contraction in Spain but stronger activity in Sweden.

UK: Markets rebound on easing geopolitical concerns

UK equities rebounded strongly as hopes for de-escalation in the Middle East improved investor sentiment.

The UK market remains sensitive to energy price movements, so expectations of easing tensions provided meaningful support.

Economic data showed some softening in manufacturing momentum. Purchasing Managers’ Index data was revised down to 51.0, with output falling for the first time in six months, although new orders continued to improve.

Meanwhile, the housing market showed renewed strength. House prices rose 2.2% year on year in March, marking the fastest pace since last summer.