Global equity markets advanced over the week, supported by signs of de-escalation in the Middle East, strong corporate earnings and generally reassuring economic data.

U.S. equities led the gains, while UK markets lagged global peers for the second consecutive week.

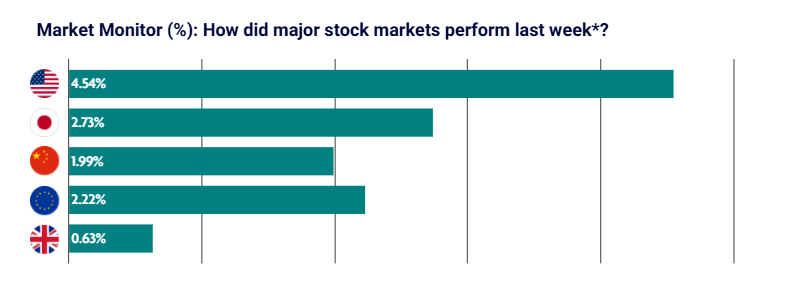

US: Equities rally on easing geopolitical tensions

U.S. equities recorded a third consecutive week of gains, with several indices reaching record highs.

The Nasdaq led performance, rising 6.84%, driven by continued strength in large-cap growth and artificial intelligence-related stocks.

Investor sentiment improved as ceasefire developments between the U.S. and Iran reduced immediate geopolitical risks. This was reinforced by confirmation that the Strait of Hormuz remained open to commercial shipping.

The first wave of first-quarter earnings reports from major banks was well received, with broadly positive commentary on economic conditions.

Economic data was also supportive. Wholesale inflation came in lower than expected, with core producer prices easing further. Jobless claims remained low, indicating continued resilience in the labour market. Regional manufacturing surveys improved, suggesting stabilising industrial activity, although housing data remained weak.

Japan: AI optimism and earnings support markets

Japanese equities moved higher, with the Nikkei 225 reaching a fresh all-time high.

Optimism around artificial intelligence, improved corporate governance and strong earnings re-emerged as key market drivers following easing geopolitical concerns.

Expectations for a near-term interest rate increase in April eased after cautious comments from Bank of Japan Governor Kazuo Ueda, who highlighted uncertainty linked to energy price shocks.

Business sentiment weakened, reflecting concerns over supply chain disruption related to Middle East tensions. However, bond yields and the yen remained relatively stable.

China: Growth holds steady but underlying momentum remains uneven

Chinese equities rebounded modestly after first-quarter GDP growth came in at 5% year on year, exceeding expectations.

Growth was supported by exports and industrial output, although underlying momentum remains uneven. Retail sales growth slowed, property investment contracted sharply and fixed asset investment remained subdued.

Trade data indicated weakening external demand, while credit growth undershot expectations despite ample liquidity, suggesting continued softness in domestic demand.

Overall, the data supports expectations of targeted policy support rather than broad-based stimulus measures.

Europe: ECB signals no urgency on interest rates

European equities continued to rise as investors responded positively to corporate earnings and confirmation that the Strait of Hormuz would remain open.

Germany’s DAX rose 3.77%, Italy’s FTSE MIB gained 2.65%, and France’s CAC 40 increased 2.0%.

The European Central Bank signalled that there is no immediate need to raise interest rates, reinforcing expectations of a prolonged pause in policy tightening.

Economic data remained mixed. Eurozone industrial production surprised to the upside, while the International Monetary Fund reduced its 2026 growth outlook due to ongoing geopolitical risks. German wholesale inflation rose sharply, driven by higher energy and metals prices.

UK: Markets rise but continue to lag global peers

UK equities delivered positive returns but continued to lag global markets for the second week in a row.

Volatility in major energy stocks such as BP and Shell weighed on overall performance, while the UK’s limited exposure to large technology companies meant it did not benefit as strongly from the global rally in AI-related stocks.

Economic data was more encouraging. The UK economy grew by 0.5% month on month in February, exceeding expectations and marking an acceleration from January.

However, the International Monetary Fund lowered its 2026 growth forecast for the UK to 0.8%, down from 1.3%. This represented the largest downward revision among G7 economies.