Global equity markets delivered mixed performance last week. Gains were largely driven by artificial intelligence-related stocks in the U.S. and Japan, while European equities came under pressure as geopolitical tensions persisted and the Strait of Hormuz remained largely closed.

US: Equities reach record highs on AI strength and earnings

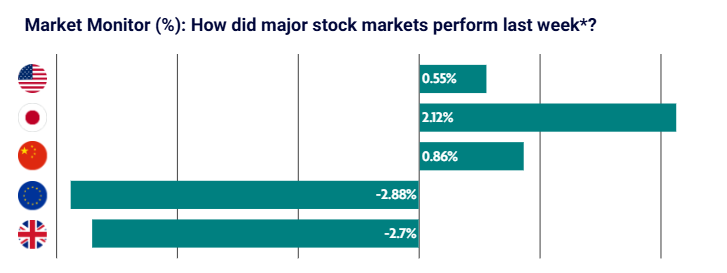

U.S. equity markets finished the week higher, with several indices reaching record highs despite ongoing geopolitical uncertainty.

The Nasdaq led gains, supported by continued strength in artificial intelligence-related stocks and generally positive corporate earnings. Around 20% of S&P 500 companies reported results during the week, with 84% exceeding expectations according to FactSet.

Markets began cautiously following recent gains but rebounded midweek after the extension of a ceasefire, even as tensions between the U.S. and Iran remained elevated.

Economic data was broadly supportive. Retail sales rose 1.7% in March, marking the strongest monthly increase since early 2023, driven by higher fuel prices and resilient consumer demand. However, consumer sentiment weakened, with the University of Michigan index falling further as inflation expectations increased.

Japan: Mixed performance as inflation rises

Japanese equities delivered mixed returns, with the Nikkei rising 2.1% while the broader TOPIX index declined 1.2%.

Technology and artificial intelligence-related stocks continued to support the Nikkei, pushing it to fresh record highs. Inflation increased in March, with core consumer prices rising to 1.8% year on year, largely driven by higher energy costs.

This has created uncertainty around the Bank of Japan’s next policy move, with markets now expecting a cautious approach at the upcoming meeting. The yen weakened against the U.S. dollar, prompting renewed speculation about potential currency intervention.

China: Policy stability supports markets

Chinese equities were broadly stable, consolidating gains following stronger-than-expected economic data in the previous week.

The CSI 300 and Shanghai Composite posted modest gains, while Hong Kong markets underperformed. The People’s Bank of China kept interest rates unchanged for the eleventh consecutive month, signalling confidence in the current growth outlook.

First-quarter GDP growth of 5% has reduced the need for immediate stimulus measures. President Xi also called for a ceasefire in the Middle East and the reopening of the Strait of Hormuz.

In corporate developments, artificial intelligence firm DeepSeek unveiled preview versions of its latest models, highlighting continued innovation within China’s technology sector.

Europe: Geopolitical tensions weigh on markets

European equities declined sharply as geopolitical risks weighed heavily on investor sentiment.

Defensive sectors such as utilities and telecommunications outperformed as the Strait of Hormuz remained largely closed and negotiations between the U.S. and Iran showed limited progress.

Losses were broad-based, with Germany’s DAX, France’s CAC 40 and Italy’s FTSE MIB all falling by more than 2%.

Economic indicators also weakened. German business confidence declined further, with the Ifo index falling to its lowest level since the pandemic. Manufacturing, trade and construction were among the weakest sectors. In France, consumer confidence dropped sharply, marking its steepest decline since the start of the war in Ukraine.

UK: Consumer confidence weakens despite resilient spending

UK equities fell over the week, with the FTSE 100 declining 2.7%, broadly in line with wider European markets.

Labour market data was mixed. The unemployment rate unexpectedly fell to 4.9%, although this was partly due to lower participation in the workforce. Retail sales were stronger than expected, rising 0.7% month on month in March, supported by fuel purchases and non-food spending.

Despite this, consumer sentiment weakened significantly. The GfK Consumer Confidence Index fell to -25 in April, the lowest level since October 2023, highlighting ongoing pressure on household confidence.