Global equity markets delivered mixed returns in a busy week for investors, with markets digesting developments in the Middle East, rising energy prices, central bank decisions and another strong wave of corporate earnings.

U.S. equities led gains, while Japanese markets lagged following a strong start to 2026.

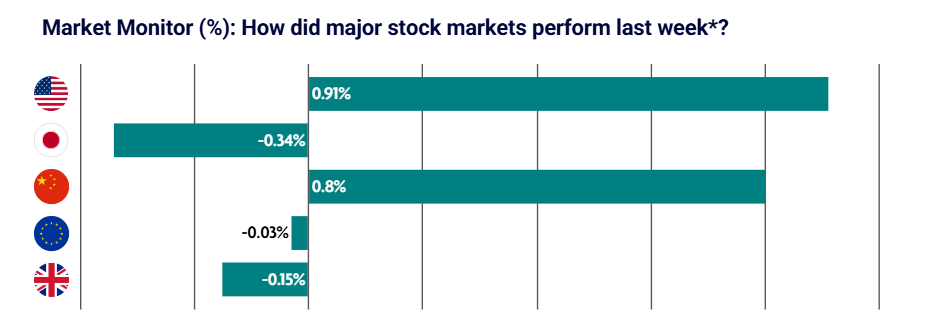

US: Equities rally on strong earnings as rates remain on hold

U.S. equities posted solid gains over the week, largely brushing aside geopolitical concerns in the Middle East and a more hawkish-than-expected Federal Reserve meeting.

Large-cap stocks outperformed, with value stocks leading growth as rising oil prices boosted the energy sector. This helped the S&P 500 deliver its strongest monthly return since November 2020.

Corporate earnings remained broadly resilient despite concerns around rising input and energy costs. Several of the “Magnificent Seven” companies reported results during the week. Alphabet rose on strong artificial intelligence demand, while Meta declined after warning of increased investment spending.

The Federal Reserve kept interest rates on hold. However, markets interpreted the meeting as more hawkish than expected due to an unusually high number of dissents. Three policymakers opposed the inclusion of easing language, while one dissented in favour of cutting rates. This marked the highest number of dissents during Jerome Powell’s time as Fed Chair.

Japan: Yen strengthens amid suspected intervention

Japanese equity markets delivered mixed performance, with the Nikkei edging slightly lower while the broader TOPIX index posted modest gains.

Currency movements dominated attention as the yen strengthened sharply, widely believed to reflect official intervention by Japanese authorities.

The Bank of Japan kept rates unchanged but delivered a more hawkish tone. A split vote highlighted growing support for further tightening, while inflation forecasts were revised higher and growth expectations lowered.

This reflects the increasingly difficult balancing act facing policymakers as they attempt to manage inflation pressures without damaging economic growth.

China: Sovereign outlook upgraded to stable

Chinese equities ended the holiday-shortened week higher following Moody’s decision to upgrade China’s sovereign outlook to stable.

Authorities continued to signal targeted policy support focused on domestic demand and strategic industries, stopping short of broad-based stimulus measures.

Industrial profits rose strongly, led by high-tech and equipment manufacturing sectors, reinforcing signs of a production and export-led recovery.

However, gains remained uneven across the wider economy, with some industries facing pressure from rising raw material costs. Overall, sentiment remained relatively stable, supported by signs of broader economic resilience.

Europe: ECB keeps rates unchanged

European equity markets were broadly flat as positive earnings momentum was offset by elevated oil prices and continued uncertainty surrounding the Middle East conflict.

Germany’s DAX rose 0.68%, Italy’s FTSE MIB gained 1.24%, while France’s CAC 40 declined 0.53%.

The European Central Bank kept interest rates unchanged but acknowledged that risks to the eurozone economy have increased. Policymakers also discussed the possibility of future tightening if inflation pressures persist.

Economic sentiment across the eurozone weakened further, falling to its lowest level since 2020. German inflation moved higher, largely driven by energy prices, while unemployment in Spain increased more than expected.

UK: Bank of England keeps rates on hold

UK equities were broadly unchanged over the week as investors remained cautious amid rising inflation and uncertain energy prices.

The Bank of England held interest rates steady at 3.75% and reiterated that it stands ready to respond if inflation pressures continue to build.

Policymakers acknowledged that inflation has moved higher, adding to concerns around household finances and the broader economic outlook.

Consumer sentiment weakened further, with confidence around retail spending falling to its lowest level on record. Overall, economic data continues to point toward a challenging backdrop for growth.