The ongoing Middle East conflict and continued energy price volatility remained the dominant drivers of investor sentiment across global markets last week.

U.S. equities were hit hardest as shifting headlines weakened confidence in a near-term resolution. UK equities proved more resilient, rebounding following the previous week’s sharp sell-off.

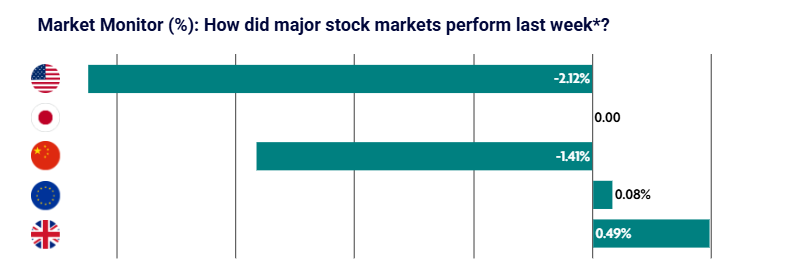

US: Escalating conflict weighs on sentiment

U.S. equities finished the week mixed and volatile, driven by ongoing developments in the Middle East and movements in oil prices.

Early optimism around a possible de-escalation faded as conflicting headlines emerged, leading to renewed uncertainty. Small and mid-cap stocks outperformed, snapping a four-week losing streak, while the S&P 500, Dow and Nasdaq declined for a fifth consecutive week. Large-cap value stocks continued to outperform growth.

Economic data pointed to slowing activity alongside rising inflation pressures. Flash Purchasing Managers’ Index data weakened, driven primarily by the services sector, while input costs rose sharply due to higher energy prices.

Jobless claims remained stable, but consumer sentiment fell and near-term inflation expectations increased. Treasury markets were broadly flat, although volatility rose as investors priced in higher inflation risks. High-yield credit markets also remained largely unchanged.

Japan: Government releases oil reserves to support markets

Japanese equities delivered mixed performance, with the Nikkei 225 broadly flat and the TOPIX index rising 1.1%.

Rising oil prices continued to weigh on sentiment given Japan’s reliance on imported energy. In response, the government released oil reserves and signalled further intervention if supply risks increase.

The yen remained close to levels that previously prompted intervention, keeping foreign exchange risks elevated. Core inflation eased slightly, supported by energy subsidies, although upward pressure from rising oil prices remains a concern.

China: Energy pressures weigh on earnings outlook

Chinese equities declined as higher oil prices raised concerns about corporate earnings, particularly across energy-sensitive sectors.

Authorities moved to cap domestic fuel price increases to limit the inflationary impact on consumers. Trade tensions with the U.S. resurfaced as China launched investigations into U.S. trade practices ahead of a potential meeting between President Xi and President Trump. Earlier in the week, Beijing had signalled a more conciliatory tone.

Industrial profits showed strong growth earlier in the year, suggesting an improving earnings backdrop prior to the escalation of the Middle East conflict.

Europe: Growth concerns increase as conflict continues

European equities were broadly flat as investors continued to assess the economic impact of the Middle East conflict.

Germany’s DAX fell 0.29%, Italy’s FTSE MIB rose 1.26%, and France’s CAC 40 gained 0.47%.

The European Central Bank indicated it remains prepared to raise interest rates if inflation pressures persist. However, policymakers stressed that it is still too early to fully assess the long-term economic impact of the conflict.

Economic data pointed to some softening in activity. Eurozone Purchasing Managers’ Index data weakened, new orders contracted and supply chain disruption increased. German business confidence also declined, despite some improvement in manufacturing.

The Organisation for Economic Co-operation and Development downgraded its growth outlook for the eurozone, reflecting increased uncertainty.

UK: Markets stabilise despite weaker growth outlook

UK equities rose 0.49% during the week, showing resilience after the previous week’s sharp decline.

Inflation remained unchanged at 3%, although this data does not yet reflect the latest rise in energy prices linked to geopolitical tensions.

The OECD downgraded its UK growth forecast significantly, warning that the UK could face the largest economic impact from the Middle East conflict among G20 nations. Its 2026 growth forecast was reduced to 0.7% from 1.2%.

The OECD also expects inflation to rise to around 4% due to higher energy prices. As a result, the combination of weaker growth and rising inflation may lead the Bank of England to keep interest rates on hold throughout 2026, with rate cuts potentially resuming in early 2027.