Strong corporate earnings supported a broad-based rally in global equity markets last week, with continued strength in the technology sector helping drive performance across major regions.

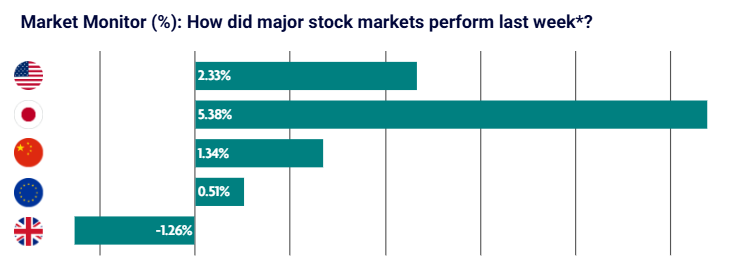

The U.S. and Japan led gains, while UK equities lagged amid fading optimism surrounding a potential U.S.-Iran peace deal and renewed geopolitical uncertainty.

US: Technology sector continues to lead gains

U.S. equities rallied over the week, supported by another strong earnings season.

Around 85% of S&P 500 companies have now reported results, with close to 85% beating expectations. Technology stocks once again led gains, driven by continued optimism around artificial intelligence-related demand.

Economic data painted a mixed picture. Jobless claims remained low and payroll growth exceeded expectations, although labour force participation fell to its lowest level since 2021. The unemployment rate held steady at 4.3%.

Productivity growth slowed in the first quarter, suggesting some moderation in economic momentum. Meanwhile, construction spending and factory orders were stronger than expected, partly driven by ongoing demand for AI infrastructure.

Despite this, consumer sentiment fell to a record low, highlighting continued pressure from higher prices and tariff concerns.

Japan: Nikkei reaches another record high

Japanese equities rallied strongly during the shortened trading week, with the Nikkei 225 reaching fresh record highs.

Technology and semiconductor stocks drove gains as optimism around global AI demand continued to support sentiment. Easing geopolitical tensions also helped reduce concerns surrounding elevated energy costs.

The yen remained volatile amid ongoing speculation about possible policy intervention.

Economic data showed real wages rising for a third consecutive month, suggesting improving domestic conditions and a more sustainable wage inflation cycle. This strengthens the case for the Bank of Japan to continue gradually normalising monetary policy.

China: Domestic demand supports equities

Chinese equities advanced following the holiday period, led by gains in technology and consumer-related sectors.

Economic data suggested resilient domestic demand, with services activity expanding faster than expected despite weaker export orders.

Investor sentiment improved on signs of stabilisation in U.S.-China trade relations ahead of upcoming high-level talks.

However, consumer behaviour remains cautious. While holiday travel volumes increased, spending per trip declined slightly, highlighting an uneven recovery in consumption.

Overall, markets continue to balance improving domestic conditions with ongoing geopolitical and external risks.

Europe: Earnings support markets despite trade concerns

European equities delivered modest gains overall, supported by easing geopolitical tensions earlier in the week and generally strong corporate earnings.

Germany’s DAX rose 0.19%, Italy’s FTSE MIB gained 2.16%, while France’s CAC 40 was broadly unchanged.

Sentiment weakened later in the week following renewed tariff threats from the U.S. towards the European Union.

Economic data remained mixed. Producer prices across the euro area rose sharply, largely driven by energy costs. Germany recorded strong factory order growth, suggesting improving industrial demand, although construction activity weakened significantly.

The European Central Bank also signalled that further interest rate increases remain possible if inflation does not continue to improve.

UK: Equities weaken amid political and energy concerns

UK equities underperformed over the week, with the FTSE 100 declining as global trade tensions and rising oil prices weighed on sentiment.

Economic data was more encouraging. The composite Purchasing Managers’ Index rose to 52.6 in April, indicating a return to moderate expansion across manufacturing and services activity.

However, political uncertainty increased following significant losses for Labour in local elections, contributing to elevated bond market volatility and concerns around future policy direction.

Overall, the data suggests the UK economy remains resilient domestically, although external pressures continue to weigh on investor confidence.