Global equity markets remained under pressure last week as the ongoing conflict in the Middle East continued to influence investor sentiment. Concerns about elevated energy prices and the potential inflationary impact have kept markets cautious.

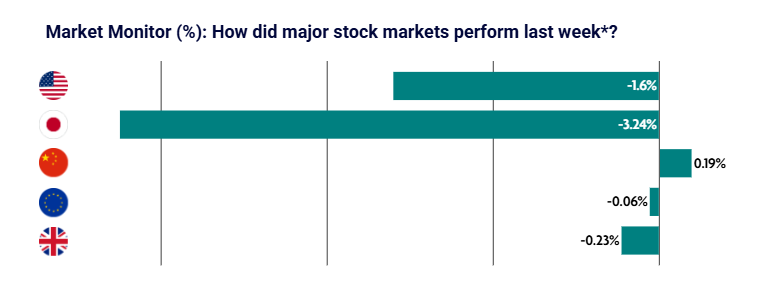

Japanese equities experienced the largest declines during the week, while Chinese markets held up comparatively better following stronger economic data.

US: Equity sell-off intensifies as Middle East conflict weighs on sentiment

U.S. equities declined for a third consecutive week as the ongoing Middle East conflict and volatile oil prices weighed on investor confidence.

Markets are balancing the risk of potential supply disruptions through the Strait of Hormuz — a critical shipping route responsible for approximately 20–25% of global seaborne oil supply — against signs that tensions may eventually ease.

Additional concerns surrounding private credit markets and trade policy also contributed to the market sell-off. The S&P MidCap 400 and the Dow Jones posted the largest declines, while the technology-heavy Nasdaq proved more resilient.

Inflation data continued to show upward pressure. Core Consumer Price Index inflation rose 0.2% in February, while core Personal Consumption Expenditure (PCE) inflation increased 0.4% in January. The annual PCE rate climbed to 3.1%, its highest level since early 2024.

Meanwhile, fourth-quarter U.S. GDP growth was revised down to 0.7% from the initial estimate of 1.4%, reflecting weaker exports, consumption, government spending and investment.

Japan: Rising oil prices pressure Japanese equities

Japanese equities declined as investors reacted to the economic impact of rising oil prices.

In response, the government announced plans to release part of its strategic oil reserves and provide fuel subsidies to help contain domestic energy costs. Japan remains highly dependent on imported energy, making it particularly sensitive to global price movements.

The Japanese yen also weakened further, raising concerns about higher import-driven inflation. The currency has approached levels that previously triggered government intervention, prompting officials to issue fresh warnings about excessive market movements.

Despite these concerns, Japan’s economic outlook showed some positive signs. Fourth-quarter GDP growth was revised up to an annualised 1.3%, supported by stronger business investment and consumer spending.

China: Stronger economic data supports markets

Chinese equities remained relatively stable as stronger-than-expected economic data helped support investor sentiment.

Exports surged by more than 21% across January and February, driven by strong global demand for technology products linked to artificial intelligence, despite weaker shipments to the United States. Imports also rose by nearly 20%, pushing the trade surplus to a record level.

Consumer inflation increased to 1.3% year on year, the fastest pace in over three years, partly driven by Lunar New Year travel demand. Core inflation also reached its highest level since 2019.

However, producer prices remained in deflation for the 41st consecutive month, although the pace of decline slowed due to stronger metals and oil prices.

Chinese technology stocks also gained following reports of increased adoption of an open-source AI agent known as OpenClaw, though enthusiasm cooled after regulators signalled caution over its use.

Europe: Rising energy costs raise concerns for growth

European equities came under pressure as investors assessed the potential economic impact of higher energy prices.

Among the major indices, Germany’s DAX closed down 0.61%, France’s CAC 40 fell 1.03%, while Italy’s FTSE MIB recorded a modest gain of 0.37%.

European Central Bank President Christine Lagarde indicated that policymakers remain prepared to respond to inflation pressures linked to rising energy costs. She also suggested that Europe may be better positioned to manage the current shock than in previous energy crises.

Economic data was less encouraging. German factory orders declined sharply on a monthly basis and exports weakened. Eurozone industrial production also fell more than expected, marking the largest monthly decline since April 2025.

UK: Economic growth stalls in January

In the UK, equity markets continued to be heavily influenced by developments in the Middle East, with investors closely monitoring oil price movements.

There is growing concern that sustained increases in energy prices could delay or limit future interest rate cuts from the Bank of England.

Latest figures from the Office for National Statistics showed that UK economic activity stalled in January, with zero growth recorded. This was below expectations for a 0.2% increase and followed only modest growth of 0.1% in December.

Service sector output was also flat, as gains in wholesale and retail trade were offset by declines in administrative and support services.

Attention will now turn to the Bank of England’s upcoming interest rate decision, with markets currently expecting no change in policy.