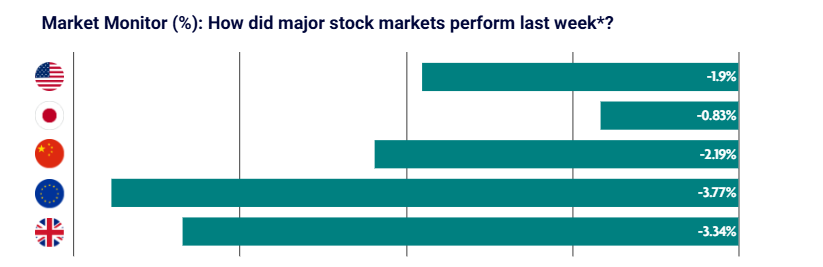

Global equity markets sold off sharply last week as attacks on key energy infrastructure and fears of a prolonged conflict in the Middle East pushed energy prices higher.

Central banks remain in a wait-and-see position, but markets have begun pricing in the possibility of further interest rate increases, particularly in the UK.

US: Federal Reserve holds rates amid rising inflation uncertainty

U.S. equities ended the week lower following a volatile period driven by the Middle East conflict, rising oil prices and renewed inflation concerns.

Energy was the standout sector within the S&P 500 as oil prices surged. The Federal Reserve held interest rates steady for a second consecutive meeting at 3.5% to 3.75%.

Policymakers continue to expect one rate cut this year, but forecasts for both inflation and economic growth were revised higher. Chair Jerome Powell highlighted the risk that escalating tensions in the Middle East could trigger an energy shock and disrupt inflation expectations.

Producer price inflation accelerated in February and exceeded expectations, raising concerns that progress on inflation may stall.

Gold fell by approximately 10% over the week, marking its worst performance since 2011, as investors reassessed economic risks linked to the conflict. Losses extended further into the following week.

Japan: Bank of Japan holds rates and warns of renewed inflation pressure

Japanese equities declined during a shortened trading week as rising oil prices and geopolitical instability weighed on sentiment.

The Bank of Japan kept its policy rate unchanged, although one policymaker voted in favour of a rate increase. The central bank warned that higher energy costs could push inflation higher again while also weighing on economic growth.

The yen strengthened slightly but remains historically weak. While this supports exporters, it increases the cost of imports. Trade data showed modest export growth, with strong demand from the European Union offset by weaker shipments to the United States and China.

China: Energy concerns outweigh improving economic data

Chinese equities fell as rising energy prices and ongoing concerns around domestic demand weighed on investor sentiment.

Recent economic data for January and February was slightly better than expected. Industrial production, retail sales and infrastructure investment all showed signs of improvement. The property market also displayed tentative signs of stabilisation, with slower declines in both new and resale home prices.

However, trade tensions resurfaced after China criticised new U.S. Section 301 investigations into manufacturing policies, which could lead to further tariffs later this year.

Europe: ECB raises inflation outlook as energy prices rise

European equity markets declined sharply as the Middle East conflict intensified and damage to key energy infrastructure, including natural gas terminals in Qatar, pushed oil and gas prices higher.

Germany’s DAX fell 4.55%, Italy’s FTSE MIB dropped 3.33%, and France’s CAC 40 declined 3.11%.

The European Central Bank kept interest rates unchanged but warned that rising energy prices are likely to push inflation higher in the near term. Its inflation forecast for 2026 was revised up significantly to 2.6%, compared with 1.9% previously.

Eurozone trade data showed a widening deficit driven by weaker exports, particularly in machinery, vehicles and chemicals. In Germany, producer prices fell more than expected, supported by lower gas and electricity costs.

UK: Rate hike expectations increase despite economic pressure

UK equities also fell sharply as global energy and geopolitical concerns outweighed domestic economic resilience.

The Bank of England held interest rates steady but signalled that a prolonged rise in energy prices could increase inflation risks and potentially justify future rate increases.

The Prudential Regulation Authority proposed new measures to strengthen bank liquidity during periods of stress. Industrial sentiment weakened, with Make UK reporting softer domestic demand and rising cost pressures.

The yield on the UK 10-year gilt has risen by 0.8% since the Middle East conflict began, putting it on track for its worst month since the 2022 mini-budget crisis.

According to the Financial Times, markets are now pricing in the possibility of up to four interest rate increases in 2026.