Global equity markets delivered another strong week of gains, supported by continued enthusiasm around artificial intelligence and growing expectations of a ceasefire agreement in the Middle East.

Japanese equities led global markets higher, while UK equities lagged due to their greater exposure to defensive and energy sectors.

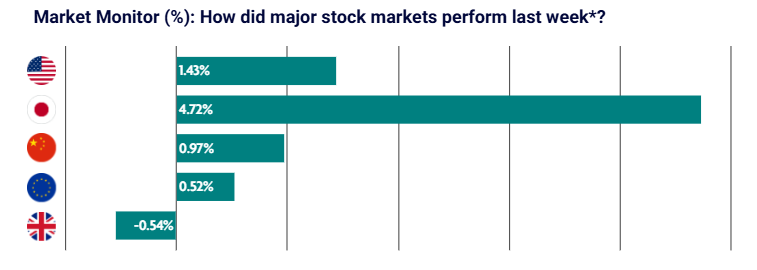

US: Equities rally on AI optimism and potential U.S.-Iran agreement

U.S. equities advanced over the holiday-shortened week, with several major indices reaching fresh record highs.

Investor sentiment improved as progress towards a potential U.S.-Iran agreement raised hopes of easing tensions in the Middle East. Falling oil prices helped reduce inflation concerns and supported broader risk appetite.

The Nasdaq led gains once again, benefiting from continued strength in AI-related stocks. The S&P 500, Russell 2000 and mid-cap indices also delivered solid returns.

Inflation data sent mixed signals. Headline Personal Consumption Expenditures (PCE) inflation eased on a monthly basis but remained higher year on year, while core inflation continued to run above target.

Federal Reserve officials maintained a cautious tone, suggesting monetary policy may need to remain restrictive for longer given persistent inflation risks.

Economic data was mixed overall. GDP growth was revised lower, although durable goods orders remained strong. Falling Treasury yields also helped support equity valuations.

Japan: Equities surge on ceasefire hopes

Japanese equities were among the strongest performers globally, with the Nikkei reaching new record highs.

The rally was driven by easing concerns around energy prices, an important factor for an economy heavily reliant on imported energy. Progress towards a U.S.-Iran agreement reduced inflation concerns and supported both equity and bond markets.

Technology and semiconductor stocks led gains, benefiting from ongoing global demand for AI-related infrastructure and services.

Inflation data came in softer than expected, with Tokyo core Consumer Price Index inflation continuing to decelerate and remaining below the Bank of Japan’s target. This has increased uncertainty around the timing of any further interest rate rises.

China: Industrial profits accelerate

Chinese equities moved higher as strong industrial profit growth supported investor sentiment.

Industrial profits increased by 24.7% year on year in April, driven by resilient external demand and improved pricing across sectors such as energy and materials.

However, gains were partially offset by renewed regulatory pressure on offshore brokerages, which weighed on Hong Kong-listed shares.

The uneven nature of China’s recovery remains a key theme. While industrial activity continues to strengthen, weakness persists across consumer-facing industries and the property sector.

Regulatory developments also continue to create uncertainty, particularly around cross-border investment access.

Europe: Modest gains as energy prices ease

European equities delivered modest gains during the week as investors responded positively to falling energy prices and hopes for easing tensions in the Middle East.

Major markets across Germany, France and Italy all moved higher, although gains were more subdued than those seen in the U.S. and Japan.

European Central Bank commentary remained a headwind. Policymakers highlighted that energy-related inflation pressures have been more persistent than expected, and minutes from the latest meeting suggested that another rate increase remains possible.

Economic data remained mixed. German unemployment edged lower, although forecasts still point towards a gradual rise in unemployment levels over the coming months.

UK: Energy and defensive sectors weigh on performance

UK equities underperformed global peers, with the FTSE 100 declining over the week.

The market’s heavier weighting towards energy and defensive sectors proved a disadvantage as oil prices fell and investors rotated into higher-growth areas of the market.

The late May bank holiday also contributed to lower trading volumes.

Inflation data was mixed. Shop price inflation surprised slightly to the upside, driven by higher shipping and input costs, partly linked to continued disruption in the Middle East.

However, food inflation continued to moderate, providing some evidence that consumer price pressures may be easing.