Global equity markets came under pressure last week as ongoing geopolitical tensions pushed bond yields sharply higher.

Technology stocks weakened as investors rotated into energy and other sectors expected to benefit from a higher interest rate environment.

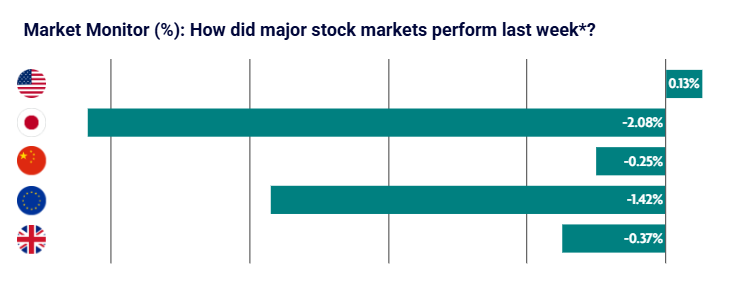

US: Inflation surprises to the upside as bond yields rise

Most major U.S. equity indices ended the week lower as renewed inflation concerns, rising bond yields and higher oil prices weighed on sentiment.

The S&P 500 briefly reached a record high before pulling back to finish broadly flat. Energy stocks led gains, while consumer discretionary, real estate and materials lagged.

Inflation data reinforced the challenge facing the Federal Reserve. Headline Consumer Price Index inflation rose 0.6% month on month and 3.8% year on year, both above expectations. Core inflation also surprised to the upside.

Producer prices surged, highlighting persistent cost pressures across the economy, largely driven by higher energy prices.

U.S. Treasury yields moved higher, with the 10-year yield reaching approximately 4.6%, reflecting growing expectations that further interest rate rises may still be required.

Retail sales remained steady but showed signs of moderation, while jobless claims edged slightly higher, suggesting a resilient but gradually cooling consumer backdrop.

Japan: Bond yields hit highest level since 1997

Japanese equities delivered mixed performance, with the Nikkei 225 declining while the broader TOPIX index advanced.

Investors rotated away from semiconductor and AI-related stocks into financials and value sectors, which tend to benefit from higher bond yields.

Japan’s 10-year government bond yield reached its highest level since 1997 amid increasing expectations of a future rate hike. Despite this, the yen weakened further against the U.S. dollar.

Rising oil prices continued to create concern around import costs and consumer spending given Japan’s heavy reliance on imported energy.

Economic data also pointed to increasing pressure on households, with input prices rising strongly while household spending fell more than expected.

China: Stable relations but limited policy progress

Chinese equities finished the week slightly lower as early optimism surrounding the Trump-Xi summit faded.

The meeting reinforced expectations of stable relations between the two countries, with commitments to continued dialogue and trade cooperation. However, markets were disappointed by the lack of any major policy breakthroughs.

Economic data remained relatively resilient. Services activity strengthened and exports rose strongly, supported by both external demand and domestic activity.

Inflation increased, particularly at the producer level, driven by higher commodity prices and continued investment linked to artificial intelligence infrastructure. This reduced expectations for any near-term policy easing.

Europe: Geopolitical concerns outweigh earnings strength

European equities declined over the week despite broadly solid corporate earnings.

Germany’s DAX fell 1.59%, Italy’s FTSE MIB declined 0.35%, and France’s CAC 40 dropped 1.97%.

Ongoing concerns surrounding stalled U.S.-Iran talks added to fears of renewed inflation pressures and tighter monetary conditions.

Economic data was mixed. Eurozone industrial production rose modestly but missed expectations as weakness in energy and consumer goods offset gains in capital and intermediate goods.

France’s unemployment rate increased to 8.1%, the highest level since 2021, highlighting continued fragility within the labour market.

UK: Political uncertainty weighs on sentiment

UK equities edged lower amid political uncertainty and weakening retail data.

Pressure on Prime Minister Keir Starmer intensified during the week, contributing to softer investor sentiment and weakness in sterling.

Economic data highlighted continued pressure on consumers. Retail sales fell 3.0% year on year in April, significantly below longer-term averages.

Business investment provided a more positive signal. UK business investment growth was 11% higher in the first quarter of 2026 compared with the end of 2019, although this remains significantly behind the 28% increase seen in U.S. non-residential investment over the same period.