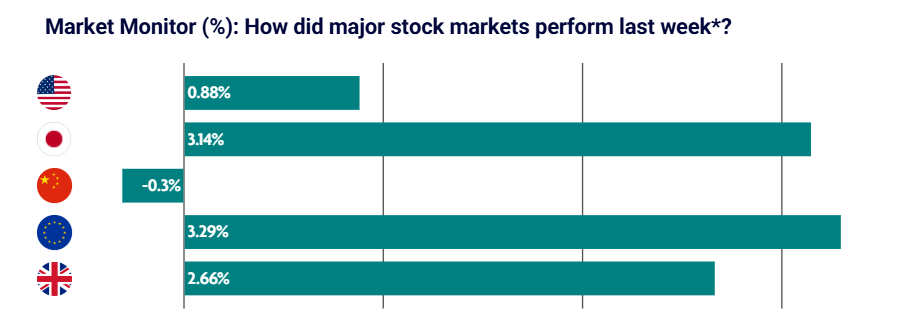

Global equity markets performed strongly last week, supported by continued momentum in artificial intelligence-related stocks and easing geopolitical tensions in the Middle East.

European equities led gains, while Chinese markets lagged amid ongoing concerns around economic growth.

US: Consumer sentiment falls to record low despite market rally

U.S. equities moved higher over the week, with the Dow Jones reaching a record high and the S&P 500 extending its recent winning streak.

Markets were supported by strong momentum in artificial intelligence-related stocks following NVIDIA earnings, alongside easing geopolitical concerns as investors increasingly favoured diplomacy over escalation in the Middle East.

Market breadth improved notably, with small-cap and value stocks outperforming and equal-weighted indices leading gains, suggesting the rally is broadening beyond large technology names.

Economic data pointed to modest growth. Purchasing Managers’ Index readings showed stronger manufacturing activity but softer services performance. Inflation pressures intensified, with input and selling prices rising at the fastest pace since 2022.

Consumer sentiment fell to a record low as cost-of-living concerns deepened and inflation expectations moved higher, reinforcing the difficult balancing act facing the Federal Reserve.

Minutes from the latest Federal Reserve meeting showed policymakers remain concerned about persistent inflation and are still open to further tightening if necessary.

Japan: Higher bond yields continue to pressure markets

Japanese equities delivered mixed performance over the week.

The Nikkei 225 declined, while the broader TOPIX index advanced as investors rotated away from semiconductor and artificial intelligence-related stocks into financials and value sectors, which tend to benefit from higher bond yields.

Japan’s 10-year government bond yield reached its highest level since 1997 amid growing expectations of a future rate increase.

The yen weakened further against the U.S. dollar despite rising yields, while higher oil prices continued to raise concerns around import costs and consumer spending.

Economic data highlighted ongoing strain on households, with input prices rising strongly and household spending falling more than expected.

China: Stable relations but limited policy progress

Chinese equities ended the week slightly lower as optimism surrounding the Trump-Xi summit faded.

The meeting reinforced expectations of stable diplomatic and trade relations, but markets were disappointed by the absence of major policy breakthroughs.

Economic data remained relatively resilient. Services activity strengthened and exports rose strongly, supported by both external demand and domestic activity.

Inflation pressures also increased, particularly at the producer level, driven by higher commodity prices and investment demand linked to artificial intelligence infrastructure. This reduced expectations for near-term policy easing.

Europe: Strong markets despite ongoing geopolitical concerns

European equities delivered strong gains overall, supported by easing geopolitical tensions and continued momentum in global markets.

Investors remained focused on inflation and interest rate expectations, while also monitoring developments surrounding U.S.-Iran negotiations.

Economic data across the eurozone remained mixed. Industrial production rose modestly, although growth continued to vary significantly between sectors and regions.

Inflation pressures linked to energy prices remain an ongoing concern for policymakers, while labour market conditions across parts of Europe continue to soften.

UK: Political uncertainty continues to weigh on sentiment

UK equities underperformed global peers over the week as political uncertainty and weaker consumer demand continued to weigh on sentiment.

Pressure on Prime Minister Keir Starmer intensified, contributing to weakness in sterling and increased investor caution.

Retail sales fell 3.0% year on year in April, highlighting continued pressure on household spending despite broader resilience elsewhere in the global economy.

Business investment growth remained positive, with investment up 11% compared with pre-pandemic levels. However, this still trails significantly behind the pace of investment growth seen in the United States.