Global markets experienced sharp swings this week following the attack in Iran, with energy prices surging and equities falling across most regions. Oil rose by around 20%, gas prices jumped roughly 60%, and both global equities and bonds declined.

These types of market moves are common during major geopolitical events. They often reflect uncertainty rather than long-term economic damage. Investors are now closely watching how the conflict develops and what impact it could have on energy markets, economic growth and inflation.

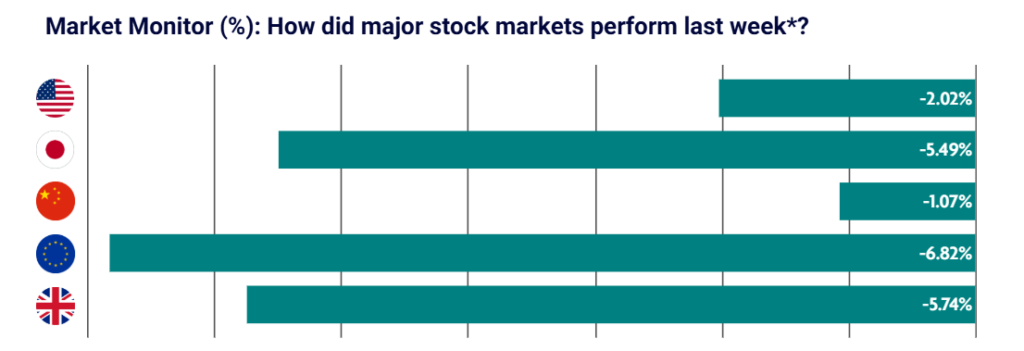

US: Middle East conflict and mixed economic data

Investors digested escalating conflict in the Middle East following U.S. and Israeli military strikes on Iran, alongside rising energy-driven inflation risks and mixed economic data.

Oil prices surged amid concerns about potential supply disruptions. Uncertainty around the duration of the conflict and its possible impact on global energy markets also influenced U.S. bond markets, as investors reassessed inflation risks and the outlook for interest rates.

Recent economic data provided mixed signals. Factory and services activity continued to expand in February, suggesting the broader economy remains resilient. However, employment data was less clear-cut. Some reports indicated companies were adding jobs and layoffs were falling, while the official government report showed a surprise decline in employment alongside a slight rise in the unemployment rate.

Japan: Investors watch oil prices closely

Japanese markets were volatile as investors evaluated the potential economic impact of rising oil prices, particularly given Japan’s heavy reliance on energy imports from the Gulf region.

Higher energy costs could feed into inflation and influence monetary policy decisions. The Bank of Japan reiterated that it will continue raising interest rates if economic growth and inflation develop in line with expectations.

Meanwhile, the yen weakened further, prompting the government to signal it may intervene in currency markets if needed.

Domestically, there are early signs that wage growth could continue. Major labour unions are requesting pay increases similar to last year, a development the central bank hopes will support a healthier cycle of stronger wages, increased spending and sustainable economic growth.

China: Conflict adds uncertainty to economic outlook

Chinese markets retreated as investors weighed the implications of the Middle East conflict alongside Beijing’s newly announced economic priorities for 2026.

China has set a growth target that reflects slower expansion compared with previous decades, while continuing to focus on strengthening domestic technology and manufacturing capabilities. Policymakers are aiming to boost investment through large financing programmes and targeted stimulus measures.

Recent manufacturing data revealed a mixed picture. Large domestic-focused firms are struggling with weaker demand, while smaller export-oriented companies appear to be performing better. Overall, China is preparing for a more challenging global environment and is aiming to support growth through targeted policy measures.

Europe: Energy concerns cloud inflation outlook

Investor sentiment weakened across Europe following the escalation of the Middle East conflict.

Rising oil and gas prices have increased concerns that higher energy costs could slow economic growth while pushing inflation higher again. Even before the latest developments, eurozone inflation had begun to rise, and markets are now considering the possibility that the European Central Bank may need to tighten policy further.

Despite these concerns, the region’s labour market remains resilient. Unemployment unexpectedly fell to a record low, highlighting continued strength in employment conditions across the eurozone.

UK: Middle East conflict overshadows Spring Statement

In the UK, investor focus shifted toward the potential economic implications of the conflict, particularly through its impact on energy prices and inflation expectations.

Sterling fell to its lowest level since early December, while the Office for Budget Responsibility warned that the conflict could have “very significant impacts” on the UK economy.

The geopolitical developments overshadowed the Chancellor’s Spring Statement, which largely confirmed expectations of weaker near-term growth but improving inflation and borrowing forecasts. No major policy changes were announced.

Economic data showed declining new orders in the construction sector, although the housing market remained relatively strong. According to the Halifax House Price Index, UK house prices rose 1.3% year over year in February, exceeding expectations.