The global economic backdrop was mixed last week, with shifting monetary policy expectations, geopolitical developments and tariff uncertainty. Despite varied market drivers, themes such as improving confidence in parts of Europe and Japan, firmer policy signals in the UK, and renewed risk appetite in China helped shape overall sentiment. The US was again the laggard, as we saw a continued rotation into other regions.

US: AI disruption concerns weigh on equities

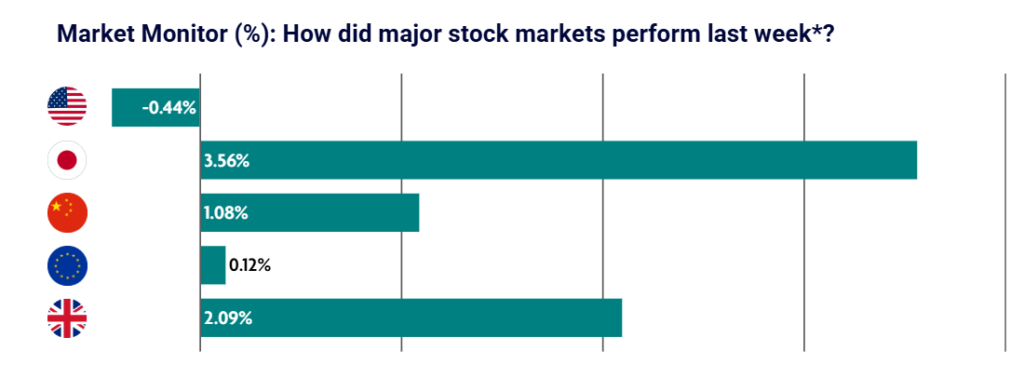

US equities fell over the week as concerns about AI-driven industry disruption and renewed trade and tariff uncertainty weighed on sentiment. The S&P 500 slipped 0.44%, despite a brief midweek improvement ahead of NVIDIA’s earnings; the chipmaker’s strong results ultimately failed to shift markets from a broader risk-off tone. Economic data added to volatility. Producer price inflation (PPI) rose 0.5% month over month, driven by a sharp increase in services prices, while factory orders fell 0.7%, largely due to weaker commercial aircraft bookings. Consumer sentiment improved modestly, with the Consumer Confidence Index rising to 91.2, though still below late-2024 highs. Meanwhile, jobless claims edged up slightly to 212,000, while continuing claims fell.

Japan: Equities rally on confidence in Japanese policy direction

Japanese markets rose sharply, with the Nikkei 225 and the broader TOPIX index both hitting record highs as investors expressed confidence in the policy direction under Prime Minister Takaichi. Markets appeared to take in stride the latest tariff announcements from the U.S., with the Bank of Japan (BoJ) Governor Kazuo Ueda noting that the 15% global tariff matches existing levies for Japan and is unlikely to have a major impact on Japan. A weaker yen and speculation about a more gradual tightening path at the Bank of Japan helped support sentiment. Tokyo’s core CPI slightly exceeded expectations, reinforcing expectations for continued BoJ policy normalisation.

China: Stocks rally in shortened trading week

Chinese equities gained in a shortened post-Lunar New Year week as risk appetite returned ahead of the upcoming “Two Sessions” meetings. Leaders typically set key economic goals at the annual legislative gathering. Holiday data showed higher total tourism spending but weaker per-trip spending, raising questions about consumption momentum. Policymakers in Shanghai eased homebuying restrictions to support the property market, while the People’s Bank of China moved to reduce the reserve requirement for FX forwards to slow the yuan’s rapid appreciation.

Europe: Rotation out of the US sees European equities well supported

European equities advanced for the week, with the EuroStoxx 600 index reaching a new high as strong corporate earnings and diversification away from the United States outweighed geopolitical and tariff concerns. Germany’s DAX, Italy’s FTSE MIB and France’s CAC 40 index all recorded gains over the week. Business confidence strengthened in Germany, while France’s main sentiment indicator slipped, highlighting divergent conditions. Inflation readings were mixed across the eurozone, with France and Spain seeing modest increases and Germany showing an easing trend.

UK: Stocks hit fresh all-time highs amid expectations for further interest rate cuts

The UK’s FTSE 100 touched a record midweek, supported by expectations of further Bank of England rate cuts following comments from MPC member Alan Taylor. Investor sentiment was also buoyed by assurances from the Trump administration that it intends to uphold the 2025 US–UK trade deal despite wider tariff uncertainty. Meanwhile, all eyes will be on Tuesday’s Spring Statement from Chancellor Rachel Reeves.