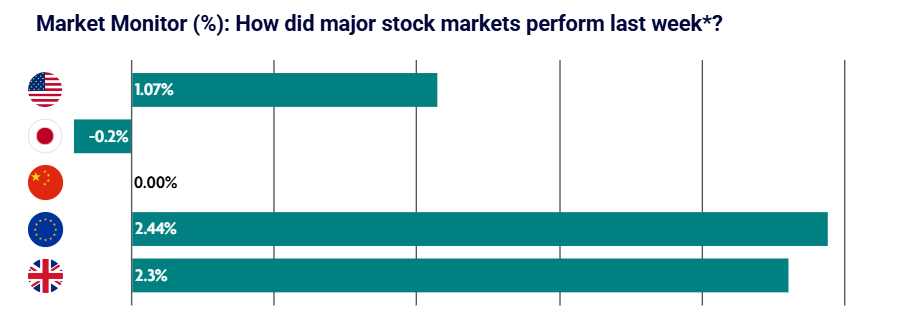

Global equities delivered a broadly positive week as supportive macroeconomic data helped underpin investor sentiment. UK and European markets extended their year-to-date outperformance versus the U.S., while Japan paused following an exceptionally strong start to 2026.

US: Policymakers split on near-term interest rate cuts

U.S. equities finished the shortened week higher, with markets rallying on Friday after the Supreme Court overturned President Trump’s global tariffs, boosting investor confidence.

The Nasdaq led gains with its first weekly rise since early January, while the S&P 500 and MidCap 400 also advanced more than 1%. However, underlying economic signals were more mixed.

Minutes from the Federal Reserve revealed a clear division among policymakers. Some officials signalled openness to further easing, while others warned that higher rates may still be required if inflation remains persistent.

Core PCE, the Fed’s preferred inflation gauge, reaccelerated to 0.4% month on month and 3.0% year on year, reinforcing concerns that disinflation may have stalled. Meanwhile, U.S. GDP slowed sharply to 1.4% in the fourth quarter as government spending, exports and consumer activity softened.

Housing data was mixed. Builder confidence and pending sales declined, though delayed Census data showed housing starts rebounding strongly at year-end.

Japan: Inflation cools to slowest pace in two years

Japanese equities eased modestly after a powerful rally earlier in the year, with the Nikkei 225 up nearly 13% year to date in local currency terms.

Geopolitical tensions weighed on global risk appetite, while domestic data suggested a softer economic backdrop. Fourth-quarter growth returned to positive territory but was significantly weaker than expected, driven by a sharp slowdown in private consumption.

Inflation cooled to 2.0% year on year, its slowest pace in two years, reflecting easing food and fuel pressures.

China: IMF upgrades 2026 growth forecast to 4.5%

Mainland Chinese markets were closed for Lunar New Year and reopened on 24 February.

During the holiday period, the International Monetary Fund upgraded China’s 2026 growth forecast to 4.5%, while emphasising the need for a structural shift toward a more consumption-led economic model.

Meanwhile, trade tensions resurfaced briefly after the U.S. published and then withdrew an updated list of Chinese companies allegedly linked to military activity. Alibaba and Baidu strongly denied the allegations. The episode added uncertainty ahead of potential future trade measures and highlighted the ongoing fragility of U.S.-China relations.

Europe: Stocks reach all-time highs on improving earnings expectations

European equities reached fresh record highs during the week, supported by improving earnings expectations, resilient macroeconomic data and a continued rotation away from tech-heavy U.S. markets.

Germany’s DAX rose 1.39%, Italy’s FTSE MIB climbed 2.29%, and France’s CAC 40 gained 2.45%.

While eurozone industrial production weakened more than expected in December, February’s PMI data surprised to the upside, with the fastest rise in new orders in nearly four years.

German investor confidence dipped from a five-year high, interrupting its recent upward momentum. Speculation surrounding European Central Bank President Christine Lagarde potentially stepping down early also added intrigue to regional politics.

UK: Equities hit all-time highs amid expectations for further rate cuts

UK equities rallied to record highs as expectations for further near-term interest rate cuts strengthened.

Inflation eased to 3.0% year on year in January, its lowest level in almost a year, partly driven by falling fuel prices. On the labour front, unemployment rose to 5.2% in the three months to December, marking a near five-year high, while wage growth slowed.

These developments have reinforced expectations that the Bank of England could begin cutting interest rates as soon as March.

Retail sales were particularly strong in January, contributing to a record £30 billion monthly trade surplus.